Auto Finance Center: A Guide to Vehicle Financing

Auto Finance Center provides essential services to car buyers by bridging the gap between desire and affordability. In an age where owning a vehicle is nearly essential, auto finance centers offer financing solutions that make it easier for buyers to drive away in the car of their dreams. Whether through loans, leases, or dealership arrangements, they serve both buyers and sellers with flexible financial options.

What Is an Auto Finance Center?

An auto finance center is a department or company that helps individuals secure financing for vehicle purchases. It may be part of a car dealership or a standalone financial institution. These centers specialize in evaluating a customer’s financial profile and connecting them with suitable financing solutions.

How Auto Finance Centers Work

Auto finance centers act as intermediaries between buyers and lenders. After assessing a buyer’s creditworthiness, income, and down payment capacity, they offer appropriate loan products. Some centers offer in-house financing, while others connect with banks, credit unions, or finance companies.

Types of Auto Financing Options

- Bank Financing: Traditional loans from banks with competitive interest rates.

- Credit Union Loans: Often lower rates and better terms for members.

- In-House Financing: Offered directly by the dealership; ideal for buyers with poor credit.

- Lease Agreements: Lower monthly payments with an option to buy at the end.

In-House vs. Third-Party Financing

In-house financing is controlled by the dealership, allowing flexibility in loan terms and approval criteria. Third-party financing, however, often comes with stricter requirements but potentially lower rates. Choosing between the two depends on credit history, down payment, and vehicle price.

Auto Finance Center Services

- Pre-approval consultations

- Loan structuring

- Credit evaluation

- Down payment assistance

- Refinancing options

- End-of-lease transitions

Loan Approval Process

The approval process involves:

- Filling out a loan application

- Providing documents (ID, income proof, address verification)

- Credit check and financial assessment

- Approval and offer generation

- Signing agreement and funding

Credit Score Impact

Your credit score plays a major role in determining interest rates and loan approval chances. Auto finance centers often work with borrowers across all credit brackets, including those with limited or no credit history.

Benefits of Using an Auto Finance Center

- One-stop solution for financing

- Multiple lender access

- Fast processing and approvals

- Guidance on improving loan terms

- Credit building opportunities

Challenges and Considerations

- Higher interest rates for poor credit

- Risk of repossession on missed payments

- Fees and hidden charges

- Shorter loan terms in in-house plans

Role of Auto Finance Centers in Car Dealerships

Most dealerships today include finance centers that help close sales by facilitating on-the-spot loan approvals. This speeds up the buying process and improves dealership revenue.

Buy Here Pay Here Financing

This type of in-house financing is common for subprime borrowers. Payments are made directly at the dealership, and approval is often quick, though interest rates can be higher.

Leasing vs Financing

Leasing offers lower monthly payments but doesn’t build equity. Financing allows ownership and builds credit over time but requires a larger commitment. Auto finance centers help buyers decide based on budget and goals.

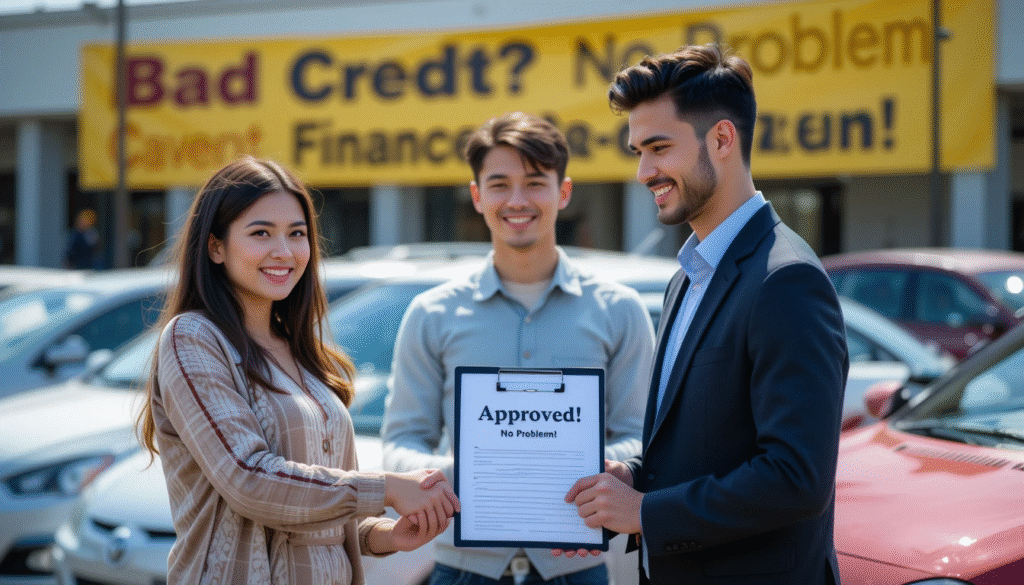

Auto Finance for Bad Credit

Special financing programs target individuals with bad credit. These may require larger down payments and higher rates but offer a chance to rebuild credit through consistent payments.

Tips for Getting Approved

- Check your credit score beforehand

- Save for a higher down payment

- Provide stable employment proof

- Choose a realistic vehicle budget

- Consider a co-signer if needed

Key Industry Trends

- Digital applications and approvals

- AI-driven credit assessments

- Subscription vehicle models

- Integration with ride-share partnerships

Choosing the Right Auto Finance Center

When selecting a provider:

- Compare interest rates

- Read reviews and testimonials

- Look for transparent fee structures

- Check loan flexibility and prepayment penalties

Regulations and Compliance

Auto finance centers must comply with:

- Truth in Lending Act (TILA)

- Fair Credit Reporting Act (FCRA)

- Equal Credit Opportunity Act (ECOA)

- State-level financial service laws

Future of Auto Financing

With the rise of fintech, expect:

- Fully digital loan processing

- Blockchain-based title transfers

- Enhanced fraud detection

- Greater personalization in loan terms

Conclusion

Auto Finance Centers are vital players in the automotive sales chain. They not only make car ownership accessible but also open financial doors for many buyers. Whether you’re a first-time car buyer or a dealership looking to grow sales, auto finance centers offer invaluable services that drive the industry forward.

FAQ’s

1. What does auto financing do?

Auto financing helps you buy a car by allowing you to borrow money and pay it back over time with interest. It makes vehicle ownership more affordable upfront.

2. What is the best place to finance a car?

Credit unions are often the best place to finance a car due to lower interest rates and flexible terms. However, banks and online lenders also offer competitive options.

3. Is it cheaper to finance through a dealership?

Financing through a dealership can be more expensive due to higher interest rates. However, special manufacturer promotions may occasionally offer better deals.

4. Which bank is best for auto financing?

Banks like Capital One, Bank of America, and Chase are known for competitive auto loan rates and easy pre-qualification. The best choice depends on your credit score.

5. Is $2000 a good down payment on a car?

A $2000 down payment is decent for a lower-priced used car. For new or more expensive cars, a larger down payment helps reduce monthly payments and interest.